All Categories

Featured

Table of Contents

Repaired or variable development: The funds you contribute to delayed annuities can expand over time., the insurance policy firm establishes a particular portion that the account will certainly earn every year.

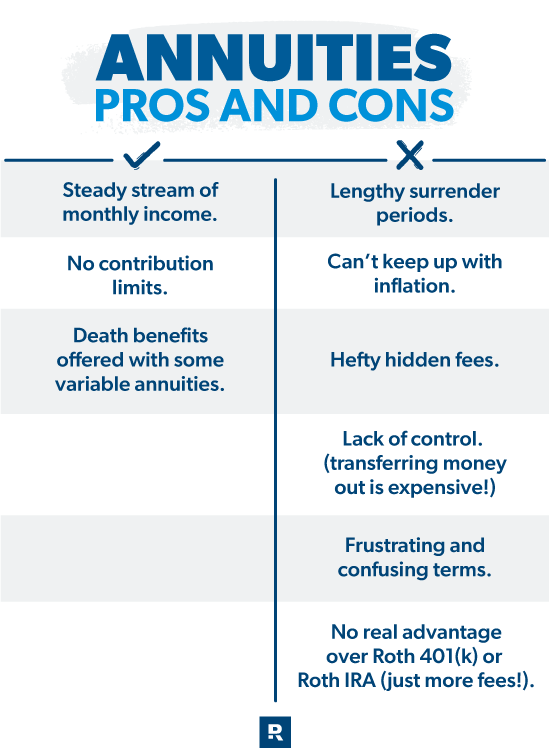

A variable annuity1, on the various other hand, is most commonly linked to the financial investment markets. The growth can be more than you would access a set price. Yet it is not ensured, and in down markets the account can decline. No. An annuity is an insurance policy item that can help assure you'll never ever run out of retirement savings.

It's normal to be worried concerning whether you've saved sufficient for retired life. Both Individual retirement accounts and annuities can assist alleviate that problem. And both can be used to construct a robust retired life strategy. Understanding the differences is vital to making the many of your savings and preparing for the retirement you are entitled to.

Over years, tiny payments can expand extensively. Beginning when you are young, in your 20s or 30s, is key to obtaining the most out of an individual retirement account or a 401(k). Annuities transform existing cost savings into guaranteed payments. If you're unsure that your savings will last as long as you need them to, an annuity is a great way to lower that problem.

On the other hand, if you're a long way from retirement, starting an individual retirement account will be helpful. And if you've contributed the optimum to your IRA and wish to place additional cash toward your retired life, a deferred annuity makes good sense. If you're unsure concerning how to manage your future financial savings, a financial professional can assist you obtain a more clear photo of where you stand.

Understanding Financial Strategies A Comprehensive Guide to Fixed Index Annuity Vs Variable Annuities What Is Fixed Annuity Vs Variable Annuity? Benefits of Variable Vs Fixed Annuities Why Choosing the Right Financial Strategy Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Variable Annuity Vs Fixed Indexed Annuity? Tips for Choosing Fixed Annuity Vs Variable Annuity FAQs About What Is A Variable Annuity Vs A Fixed Annuity Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

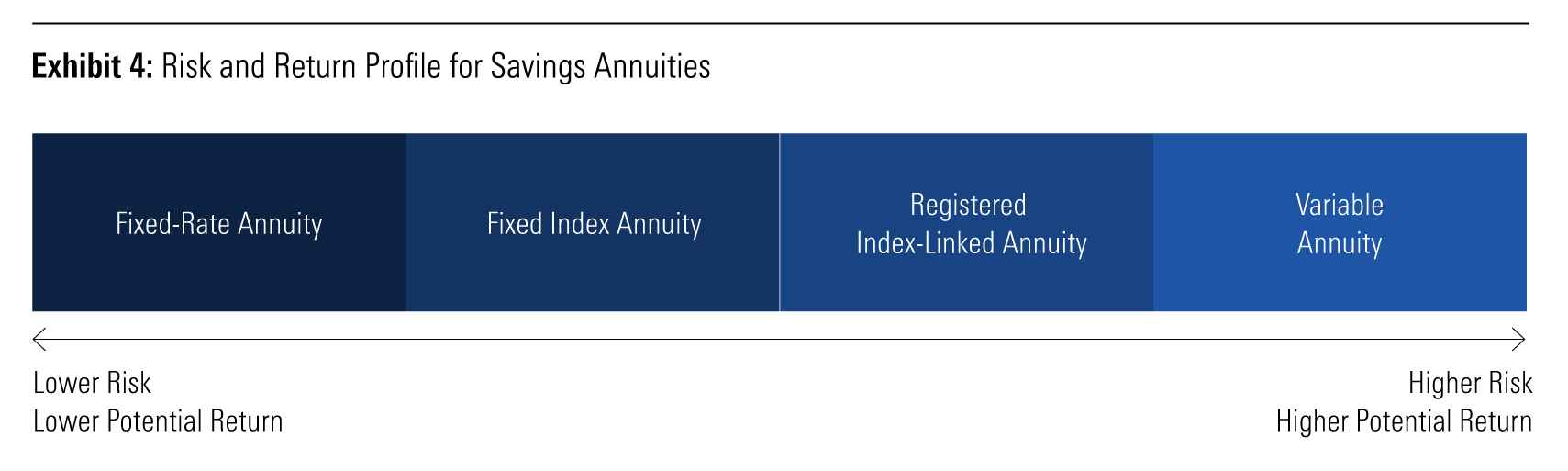

When thinking about retired life planning, it is essential to locate an approach that best fits your lifefor today and in tomorrow. may help guarantee you have the earnings you need to live the life you desire after you retire. While dealt with and taken care of index annuities sound comparable, there are some vital differences to sort through before choosing on the ideal one for you.

is an annuity agreement made for retirement income that ensures a fixed rates of interest for a specified amount of time, such as 3%, no matter of market performance. With a set rate of interest, you recognize in advance exactly how much your annuity will expand and just how much earnings it will certainly pay out.

The earnings might be available in fixed repayments over an established number of years, taken care of repayments for the remainder of your life or in a lump-sum settlement. Revenues will certainly not be exhausted till. (FIA) is a sort of annuity agreement developed to produce a steady retired life revenue and enable your possessions to expand tax-deferred.

This develops the possibility for more growth if the index executes welland conversely uses defense from loss as a result of inadequate index efficiency. Your annuity's rate of interest is connected to the index's efficiency, your money is not straight invested in the market. This suggests that if the index your annuity is linked to doesn't perform well, your annuity doesn't shed its value due to market volatility.

Set annuities have an ensured minimum passion rate so you will certainly receive some interest each year. Fixed annuities may have a tendency to position less monetary threat than other kinds of annuities and investment products whose values climb and fall with the market.

And with particular sorts of taken care of annuities, like a that set rate of interest can be secured with the whole contract term. The rate of interest earned in a fixed annuity isn't impacted by market fluctuations for the period of the fixed period. As with the majority of annuities, if you desire to take out money from your dealt with annuity earlier than scheduled, you'll likely incur a fine, or give up chargewhich occasionally can be large.

Understanding Annuities Variable Vs Fixed A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Benefits of Fixed Interest Annuity Vs Variable Investment Annuity Why Retirement Income Fixed Vs Variable Annuity Can Impact Your Future How to Compare Different Investment Plans: A Complete Overview Key Differences Between Fixed Income Annuity Vs Variable Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Choosing Between Fixed Annuity And Variable Annuity? Tips for Choosing Immediate Fixed Annuity Vs Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Vs Variable Annuities Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Tax Benefits Of Fixed Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

Furthermore, withdrawals made before age 59 might go through a 10 percent federal tax obligation fine based upon the fact the annuity is tax-deferred. The interest, if any kind of, on a set index annuity is tied to an index. Since the interest is linked to a stock market index, the passion attributed will certainly either benefit or suffer, based on market performance.

You are trading possibly taking advantage of market growths and/or not keeping pace with inflation. Dealt with index annuities have the benefit of possibly using a higher guaranteed interest price when an index executes well, and principal security when the index experiences losses. In exchange for this security versus losses, there may be a cap on the optimum earnings you can obtain, or your incomes might be restricted to a percentage (as an example, 70%) of the index's readjusted value.

It usually additionally has a present rate of interest price as declared by the insurance provider. Passion, if any, is tied to a defined index, up to an annual cap. A product could have an index account where passion is based on how the S&P 500 Index does, subject to a yearly cap.

Passion made is dependent upon index performance which can be both favorably and adversely impacted. In addition to understanding taken care of annuity vs. taken care of index annuity distinctions, there are a couple of other kinds of annuities you could desire to check out before making a decision.

{kind=link}

Table of Contents

Latest Posts

Decoding Variable Annuity Vs Fixed Annuity A Closer Look at Fixed Vs Variable Annuity Pros And Cons Defining Variable Annuity Vs Fixed Annuity Pros and Cons of Deferred Annuity Vs Variable Annuity Why

Breaking Down Fixed Annuity Vs Variable Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Retirement Income Fixed Vs Variable Annuity Advantages and Disadvantages of Diff

Decoding Fixed Vs Variable Annuity Pros Cons A Closer Look at How Retirement Planning Works What Is What Is Variable Annuity Vs Fixed Annuity? Advantages and Disadvantages of Different Retirement Plan

More

Latest Posts